If you or a loved one needs long-term care, you probably don't want to pay it from your hard-earned savings. Instead, consider purchasing a long-term care (LTC) insurance policy. As a bonus, qualified LTC policies may deliver some tax breaks. Here are answers to some frequently asked questions about this type of coverage.

How Does Long Term Care Insurance Work?

Benefits paid under an LTC policy are usually stated as daily maximums, typically ranging from $50 to $500. You choose the benefit level appropriate for your needs, and then you're reimbursed up to the amount chosen. A Long Term Care policy with a monthly benefit reimburses you for a stated amount per month, regardless of how many days you receive care or the cost of those days.

You can buy a Long Term Care policy with or without automatic annual inflation adjustments to your benefit maximums. Usually, the annual inflation adjustment rate is 3% to 5%, and that rate can be compounded annually or not. Choosing a 5% compounded inflation adjustment feature is more expensive than a 3% fixed rate option.

While lower benefits naturally translate into lower premiums, don't get carried away with cost savings. Long Term Care facilities can be surprisingly expensive. The national average cost for a semiprivate nursing home room in 2018 was $245 a day, which translates to $89,425 over a full year. A private room cost $275 a day, or $100,375 over a full year, according to a survey by seniorliving.org, an independent research database for caregivers.

Likewise, the National Center for Assisted Living (a national advocacy and education organization for the assisted living profession) estimates that the average 2018 base rate for a year in an assisted living facility was $44,000.

The average 2018 cost for nonmedical home care provided by commercial agencies was $20.50 per hour, with state averages ranging from $15 to $27.50 per hour. Private individuals can usually be hired to provide home care services for 20% to 30% less, according to senior care referral company payingforseniorcare.com.

Benefit payments commence after the policy waiting period has been satisfied. Typically, policies have waiting periods of 90 to 100 days.

Finally, you can usually choose benefit periods ranging from two years to lifetime coverage. Most policies have benefit periods of three to five years. Of course, no one is sure how long they'll need coverage. But according to the National Center for Assisted Living, the average stay in a nursing home is 835 days.

When Should I Sign Up?

When you sign up for Long Term Care insurance, the hope is that you'll pay fixed monthly premiums, based on your age and health factors at the time you enroll. Enrolling at age 65 could cost significantly more than enrolling at age 55.

Your overall health status needs to be good when you apply for coverage or you won't be accepted at any age. After you obtain coverage, it will remain in force — regardless of changes in health and age — as long as you pay the premiums.

Important: While the LTC insurance company can't raise your premiums due to changes in your age or health, it can raise premiums for broad classes of policyholders when financial results decline. This has turned out to be an all-too-common occurrence. So be sure to check the overall reputation and premium-raising history of any insurance company you're considering for Long Term Care coverage.

Are Benefits Tax-Free?

Benefits received under a qualified LTC policy are generally federal-income-tax-free (and usually state-income-tax-free, too), because they're considered insurance reimbursements for medical expenses.

For 2019, this tax-free treatment automatically applies to benefits of up to $370 per day. The tax-free cap is adjusted annually for inflation.

Even if you receive benefits above the cap, they are still tax-free as long as they don't exceed your actual costs for long term care.

If you collect LTC insurance benefits during the year, the total amount will be reported to you on Form 1099-LTC, which you should receive early in the following year. Your tax advisor can help you calculate the taxable amount of benefits and file the proper tax forms. Most people don't have to report any taxable benefits from collecting Long Term Care insurance benefits.

Can I Deduct LTC Premiums?

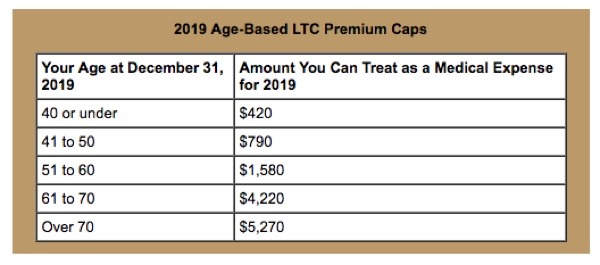

Usually yes, within limits — assuming you itemize deductions. Because qualified Long Term Care policies are considered health insurance for federal income tax purposes, the premiums are treated as medical expenses for itemized medical expense deduction purposes. Most policies issued these days are qualified. However, if your premiums for a qualified policy exceed the age-based caps listed below, you can only count the capped amount as a medical expense.

Important: Don't forget to count premiums paid for coverage on your spouse as well as premiums paid for any other dependent relative. For this purpose, a dependent relative is someone for whom you pay over half the cost of support during the year.

Add up 1) your qualified LTC insurance premium amount (limited to the age-based cap if applicable), and 2) your other medical expenses (such as health and dental insurance premiums, insurance co-payments, out-of-pocket prescription costs, and all your other unreimbursed medical outlays). If the total exceeds 10% of your adjusted gross income (AGI), you can write off the excess as an itemized medical expense deduction (assuming you have enough other types of deductions to itemize).

AGI includes all taxable income items. It's reduced by certain write-offs such as deductible IRA contributions and alimony payments required by a pre-2019 divorce agreement.

If you're self-employed, you can generally deduct premiums for qualified Long Term Care insurance whether you itemize or not. However, the age-based deduction cap also applies.

Which LTC Policies Qualify?

In order to qualify for the preferential tax treatment, Long Term Care policies must be guaranteed renewable, and they can't have any cash value. Most policies sold these days are qualified policies, but make certain before you sign up to reap these valuable tax breaks. Contact us if you have questions or want more information about LTC insurance and the related tax breaks.