Good things come to those who wait. Older taxpayers may be entitled to some age-based tax breaks. Here are the details:

Catch-Up Contributions to Retirement Accounts

Older taxpayers can make extra “catch-up” contributions each year to certain types of tax-favored retirement accounts. For the 2019 tax year, the maximum catch-up contributions are:

- $1,000 for traditional and Roth IRAs, and

- $6,000 for 401(k), 403(b) and 457 plans.

Once you've reached age 50, you can make catch-up contributions to your traditional IRA or Roth IRA. Deductible contributions to traditional IRAs create current tax savings, but your income may be too high to qualify.

Contributions to Roth IRAs don't generate any upfront tax savings. But you can take tax-free withdrawals after age 59½, assuming that you've had at least one Roth account open for more than five years. There are income restrictions on annual Roth contributions, too.

At the very least, you can make extra nondeductible traditional IRA contributions and benefit from the account's tax-deferred earnings advantage.

Assuming your company retirement plan allows catch-up contributions, you can also contribute an extra $6,000 to your 401(k), 403(b) or 457 account. If allowed under your plan, this privilege starts the year you turn age 50.

Contributions to 401(k), 403(b) and 457 accounts are subtracted from taxable wages. So, you effectively get a federal income tax deduction for making them. If your state has a personal income tax, you'll generally get a state tax deduction, too.

You can use the resulting tax savings to help pay for part of your catch-up contribution, or you can set them aside in a taxable retirement savings account to further increase your retirement-age wealth.

Catch-up Contributions Can Be Valuable

Surprisingly, many people age 50 or older fail to make retirement plan catch-up contributions. Why not? They don't realize that it can make a significant difference in their retirement-age wealth.

For example, Sam turned 50 in May. She decides to contribute an extra $1,000 to her IRA in 2019 and continues making catch-up contributions for the next 15 years, through age 65. How much extra will the catch-contributions add to her retirement nest egg by 2034?

Assuming a 4% annual return and rounding to the nearest $1,000, Sam would have added approximately $22,000 to her retirement-age wealth ($16,000 of catch-up contributions + approximately $6,000 of earnings). If Sam's annual return increased to 8%, her catch-up contributions would have added more than $30,000 to her retirement-age wealth.

Important: Making larger deductible contributions to a traditional IRA can also lower your tax bills. Making additional Roth IRA contributions won't, but you'll be able to take more tax-free withdrawals later in life.

Here's another example: Alex turned 50 in July. He decides to contribute an extra $6,000 to his company 401(k) plan for 2019 and continues making catch-up contributions for the next 15 years, through age 65.

By 2034, assuming a 4% annual return and rounding to the nearest $1,000, Alex's catch-up contributions would have added approximately $131,000 to his retirement-age wealth ($96,000 of catch-up contributions + approximately $35,000 of earnings). If his annual return increased to 8%, the catch-up contributions would have added almost $182,000 to his retirement-age wealth. Plus, larger contributions to Alex's retirement account also would lower his tax bills from 2019 through 2034.

Roth IRA Conversions

Do you expect to be in the same or higher tax bracket during future years? If so, the current tax hit from a conversion done in 2019 may be a small price to pay for avoiding potentially higher future federal income tax rates on the account's earnings.

Another reason that Roth conversions appeal to seniors is that you don't have to take annual required minimum distributions (RMDs) from Roth IRAs. An RMD is the amount you're legally required to withdraw from your qualified retirement plans and IRAs after reaching age 70½. Essentially, the tax law requires you to tap into your retirement assets — and begin paying taxes on them — whether you want to or not.

So, you can keep the Roth IRA balances at work earning more income-tax-free dollars. Finally, you can leave Roth IRAs to your heirs, and they can benefit from income-tax-free dollars earned after your death.

There's no income limit imposed on Roth conversions. Your tax advisor can help you evaluate the pros and cons of a Roth conversion.

Charitable Donations from IRAs

If you're age 70½ or older, you can make up to $100,000 in annual cash donations to IRS-approved charities directly out of your IRA. These direct donations are called qualified charitable distributions (QCDs).

QCDs are tax-free and nondeductible. So, they don't directly affect your tax bill. However, they count as withdrawals for purposes of meeting the required minimum distribution (RMD) rules that apply to traditional IRAs after age 70½.

So, if you haven't yet taken your 2019 RMDs, consider holding off and arranging tax-free QCDs before year end in place of taxable RMDs. That way you can meet your 2019 RMD obligation in a tax-free manner while satisfying your charitable goals at the same time.

Gifts of Appreciated Assets

Do you own taxable investments that have appreciated in value? Unfortunately, many older taxpayers with these types of assets are subject to the maximum federal income tax rate on long-term capital gains. That rate is currently 20% plus the 3.8% net investment income tax (NIIT) that applies at higher income levels.

To avoid the capital gains tax hit, consider gifting these investments to your loved ones in lower tax brackets. This enables you to share your wealth, plus the recipient will pay lower tax rates than you'd pay if you sold the same shares.

For example, relatives in the 0% income tax bracket for long-term capital gains and qualified dividends will pay a 0% tax rate on gains from shares that were held for over a year before being sold. (For purposes of meeting the “more-than-one-year” rule for gifted shares, you can count your ownership period plus the gift recipient's ownership period.)

Even if the appreciated shares have been held for a year or less before being sold, your relative will probably pay a much lower tax rate on the gain than you would.

For taxable investments that are currently worth less than what you paid for them, consider selling the shares to claim the resulting tax-saving capital loss for yourself. You can give the cash sales proceeds to your relative.

Medical Expense Deductions

If you're 65 or older, you may have fallen into the habit of automatically claiming the standard deduction instead of itemizing. Taking the standard deduction is often the right way to go, but not always.

Many older people incur significant medical costs. These expenses can be deducted if you itemize and your medical costs exceed 10% of your adjusted gross income (AGI). AGI includes all taxable income items and certain write-offs such as deductible IRA contributions.

What medical expenses qualify? Insurance co-payments, deductibles, dental visits, eye exams, wheelchairs, glasses and other out-of-pocket medical costs count as medical expenses for itemized deduction purposes.

In addition, Medicare insurance premiums count as health insurance premiums for purposes of the itemized deduction for medical expenses. Specifically, premiums for Medicare Parts A, B, C, and D, as well as premiums for Medigap coverage, qualify.

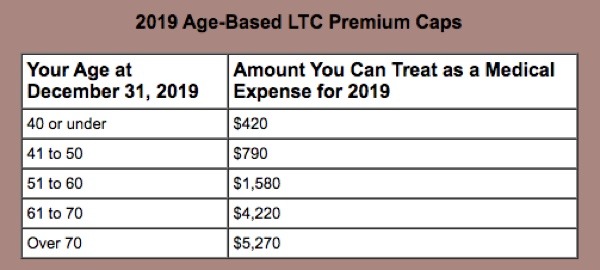

Premiums for qualified long-term care (LTC) insurance also count as medical expenses for itemized deduction purposes. For 2019, they're subject to the following age-based limits:

If you (and your spouse) have enough medical expenses to exceed the 10%-of-AGI threshold, you'll need to consider other categories of itemized expenses that you'll have incurred by year end, such as

- State and local income and property taxes (or state and local general sales taxes if you to choose to claim them instead of state and local income taxes),

- Qualified residence interest on a first or second home, and

- Charitable donations.

Add other itemizable expenses to your medical expense deduction and see if the total exceeds the applicable standard deduction amount. 2019 standard deduction amounts are as follows:

- $13,850, if you're unmarried and you'll be 65 or older at year end,

- $12,200, if you're unmarried and you'll be under 65 at year end,

- $27,000, if you file jointly and both spouses will be 65 or older at year end,

- $25,700, if you file jointly and one spouse will be under 65 at year end,

- $24,400, if you file jointly and you'll both be under 65 at year end,

- $20,000, if you use head-of-household filing status and you'll be 65 or older at year end, or

- $18,350 if you use head-of-household filing status and you'll be under 65 at year end.

If your total itemized deductions exceed your allowable standard deduction, you should itemize deductions on your 2019 federal income tax return.

Discuss Your Options with a Qualified Professional

With age comes wisdom — and some possible tax saving strategies. Contact your tax advisor to discuss these and other ideas to help lower your tax bill.

Avoiding the Estate Tax Clawback

In late 2018, the IRS issued proposed regulations that would allow individuals who make large gifts from 2018 to 2025 to benefit from the generous unified federal gift and estate tax exemption for those years. The regulations stipulate that taxpayers wouldn't be penalized if the exemption reverts to the lower amount allowed under prior law.

For 2018 through 2025, the Tax Cuts and Jobs Act (TCJA) effectively doubled the unified federal gift and estate tax exemption amount from $5 million per taxpayer to an inflation-adjusted $10 million per taxpayer. For 2019, the exemption amount is $11.4 million.

Under the proposed IRS regs, the exemption would be the greater of:

- The TCJA exemption amount that was used to shelter earlier gifts, or

- The exemption amount that's allowed in the post-TCJA year of death.

In light of this proposal, consider making big gifts sooner rather than later, while the current exemption amount is still in place. Consult your tax advisor to devise the optimal estate planning strategy for your situation.