If your small business is unincorporated, you may be fed up with paying the federal self-employment (SE) tax. This tax is how the federal government collects Social Security and Medicare taxes from self-employed individuals. However, you may be able to lower your exposure to these taxes if you structure your business as a subchapter S corporation for federal tax purposes. Here are the details on how this tax-saving strategy can work.

Employment Tax on Salary Income

First, let's review how federal employment taxes are collected for regular W-2 employees. If a taxpayer earns salaries and wages as an employee, Social Security tax will be incurred at a 12.4% rate on the first $132,900 you earn in 2019. The taxpayer's employer will withhold half (6.2%) from his or her paychecks. The other half will be paid by the employer directly to the U.S. Treasury. No Social Security tax is incurred on any salary above the $132,900 ceiling for 2019.

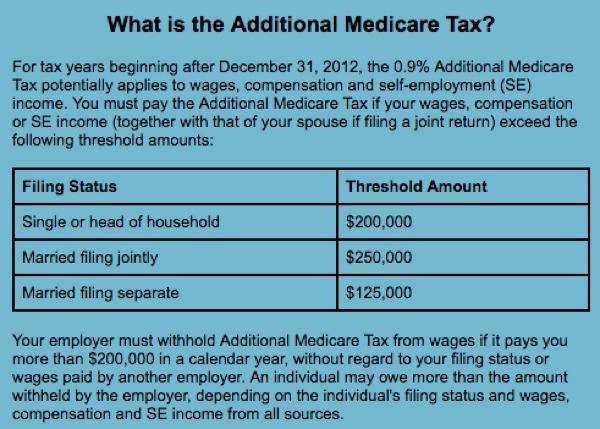

Medicare tax on salary income is incurred at a 2.9% rate before rising to 3.8% at higher salary levels. (See “What is the Additional Medicare Tax?” below.) Part of the Medicare tax is withheld from the employee's salary, and part is paid by the employer. There's no income ceiling on the Medicare tax or the 0.9% Additional Medicare Tax.

Employment Tax on SE Income

How does the situation differ if you're self-employed? For 2019, you'll pay the maximum 15.3% SE tax rate on your first $132,900 of net SE income. That includes 12.4% for the Social Security tax component and 2.9% for the Medicare tax component.

No Social Security tax is incurred on SE income above the Social Security tax ceiling of $132,900 for 2019. But the Medicare tax component continues at a 2.9% rate before rising to 3.8% at higher levels of SE income. There's no income ceiling on the Medicare tax component or the 0.9% Additional Medicare Tax.

For example, suppose your unincorporated small business generates SE income of $216,567 for you in 2019. To calculate your SE tax bill, the net SE income figure is multiplied by 0.9235 to equalize the overall tax impact of federal employment taxes on SE income and salary income.

Your business generates $200,000 of SE income after applying the 0.9235 factor. So, you'll owe $16,480 of Social Security tax ($132,900 × 0.124), plus $5,800 of Medicare tax ($200,000 × 0.029). That's a grand total of $22,280 in SE tax for 2019.

To make matters worse, your SE tax bill is likely to increase every year due to inflation adjustments to the Social Security tax ceiling (the “wage base”) and the growth of your business.

Tax on Salary Income for S Corp Shareholder-Employees

Salaries paid to employees of S corporations — including an employee who's also a shareholder — are subject to federal employment taxes just like salaries paid to a regular W-2 employee. That is, the employee owes 6.2% Social Security tax on the first $132,900 for 2019 and 1.45% Medicare tax on all salary income. These amounts are withheld from the employee's paychecks. The employer pays in matching amounts of Social Security tax and Medicare tax directly to the U.S. Treasury.

At higher salary levels, an employee (including an S corporation shareholder-employee) must pay the 0.9% Additional Medicare Tax out of his or her pocket. So, the combined federal employment tax employer rate for the Social Security tax is 12.4%, and the combined rate for the Medicare tax is 2.9%, rising to 3.8% at higher salary levels. These rates are effectively the same as the SE tax rates.

So, the bad news is that salary income for S corporation shareholder-employees is subject to federal employment tax. The good news is that S corporation taxable income passed through to a shareholder-employee and S corporation cash distributions paid to a shareholder-employee generally are not subject to federal employment taxes.

As a result, S corporations may potentially be in a more favorable position than sole proprietorships, single-member limited liability companies (LLCs) that are treated as sole proprietorships for tax purposes, partnerships and multimember LLCs that are treated as partnerships for tax purposes.

Tax Reduction Strategy

How can you lower the burden of federal employment taxes if you're interested in this strategy? First, structure your business as an S corporation. Then pay modest salaries to yourself and any other shareholder-employees. Finally, pay out the remaining corporate cash flow (after you've retained enough in the company's accounts to sustain normal business operations) as federal-employment-tax-free cash distributions.

For example, let's suppose you own an S corporation that generates net income of $200,000 before paying your $60,000 salary for 2019. Only the $60,000 salary is subject to federal employment taxes of $9,180 ($60,000 x 0.153). That's significantly less than the $22,280 federal employment tax bill in the previous example.

Caveats

Operating as an S corporation and paying yourself a modest salary will work if you can prove that your salary is “reasonable” based on market levels for similar jobs. Otherwise you run the risk of the IRS auditing your business and imposing back employment taxes, interest and penalties. That said, the risk of the IRS successfully doing that is minimal if you can demonstrate that an unrelated third party would agree to perform the same work for that same amount. Your tax advisor can help with that.

There are also some unfavorable side-effects of paying modest salaries to S corporations shareholder-employees. First, modest salaries could limit contributions to certain tax-favored retirement accounts. If the corporation maintains a SEP or garden-variety profit-sharing plan, the maximum annual deductible contribution is limited to 25% of the shareholder-employee's salary. So, the lower the salary, the lower the maximum contribution to your account. But, if the S corporation offers a 401(k) plan, generous contributions can still be made to your account while paying modest annual salaries.

In addition, paying modest salaries could reduce Social Security benefits that shareholder-employees receive at retirement. And S corporation status can trigger some tax complexities.

For example, a separate business tax return must be filed for an S corporation, and transactions between S corporations and shareholders (including transfers of business assets to the new corporation) must be evaluated for potential tax consequences. Corporations also may be subject to various formalities under state law, such as conducting board of directors' meetings and keeping minutes. Before choosing to operate as an S corporation, you'll have to consider whether the additional paperwork is worth the federal employment tax savings.

Need Help?

Contact your tax advisor if you think converting an existing unincorporated business into an S corporation could help reduce your federal employment taxes. He or she can help with the mechanics of making the initial conversion under applicable state law and then handle the post-conversion tax issues. Although the March 15 deadline for electing S status has already passed for 2019, it can still be made for 2020 and beyond.