Treasury Regulations Permit Naming Trusts as (Designated) Beneficiaries of Retirement Accounts

While often viewed as a “gray” area, the reality is that a trust can absolutely become eligible for designated beneficiary treatment, qualifying as a “see-through” trust where the post-death RMDs are calculated based on the life expectancy of the oldest of the trust's underlying beneficiaries.

While often viewed as a “gray” area, the reality is that a trust can absolutely become eligible for designated beneficiary treatment, qualifying as a “see-through” trust where the post-death RMDs are calculated based on the life expectancy of the oldest of the trust's underlying beneficiaries.

In order to be treated as a “see-through trust” and qualify as a designated beneficiary, the trust must meet four very specific requirements, as stipulated in Treasury Regulation 1.401(a)(9)-4, Q&A-5:

1) The trust must be a valid trust under state law.

This requirement is rather straightforward – the trust must be legally formed under state law. Generally this just means the trust is not a handwritten trust (not permitted in many/most states), has been properly signed and executed as a trust (witnessed, notarized, etc., as required under state law), and does not contain any provisions that would outright invalidate the trust under state law. For virtually any trust drafted by a competent attorney that was legally signed and executed in the first place, this requirement should be a non-issue.

2) The trust must be irrevocable, or by its terms become irrevocable upon the death of the original IRA owner.

A revocable living trust that becomes irrevocable upon the death of the owner should qualify under this provision, as would any irrevocable trust that was simply drafted to be irrevocable from the moment it was executed. Notably, while the rules do require that the trust beneficiary be irrevocable (or become so upon death), IRA beneficiary designations themselves remain revocable until death, which means even if an “irrevocable” trust is made as beneficiary of the IRA now, the IRA owner can still change the trust by simply creating a new irrevocable trust and changing the beneficiary designation from the old irrevocable trust to the new irrevocable trust (or alternatively, just get rid of the irrevocable trust altogether if desired).

A revocable living trust that becomes irrevocable upon the death of the owner should qualify under this provision, as would any irrevocable trust that was simply drafted to be irrevocable from the moment it was executed. Notably, while the rules do require that the trust beneficiary be irrevocable (or become so upon death), IRA beneficiary designations themselves remain revocable until death, which means even if an “irrevocable” trust is made as beneficiary of the IRA now, the IRA owner can still change the trust by simply creating a new irrevocable trust and changing the beneficiary designation from the old irrevocable trust to the new irrevocable trust (or alternatively, just get rid of the irrevocable trust altogether if desired).

Make sure the trust is properly executed to be a valid see-through trust, though (see #1 above), and be cautious about certain joint revocable trusts that may still remain revocable after the first death. Bear in mind that the IRA beneficiary “irrevocable” trust could still be a subsection of another trust that is revocable (as long as the particular sections guiding the trust-as-IRA-beneficiary cannot be revoked after death of the IRA owner), and that the trust could also be a testamentary trust created under a Will that doesn't even come into existence as an irrevocable trust until the death of the IRA owner in the first place.

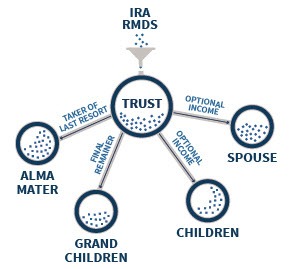

3) The trust's underlying beneficiaries must [all] be identifiable as being eligible to be designated beneficiaries themselves.

Not surprisingly, the Treasury Regulations require that if distributions are going to be stretched over the life expectancy of trust beneficiaries, the trust beneficiaries must be identifiable in the first place, which generally means they should either be identified by name, or identified as members of a “class” of beneficiaries that could be identifiable when the time comes (e.g. “my children” or “my grandchildren” would be fine, but “to whomever my trustee decides to make distributions” would not).

Notably, embedded in this requirement that all beneficiaries be identified is that they be identifiable as designated beneficiaries, which means they must be individual, living, breathing human beings as beneficiaries; if a charity or some other non-living entity is a trust beneficiary, then the trust will not be able to do a stretch over the life expectancy of the underlying beneficiaries; because not all the underlying beneficiaries as designated beneficiaries have a life expectancy in the first place!

4) A copy of “trust documentation” must be provided to the IRA custodian by October 31st of the year following the year of the IRA owner's death.

Under supporting Treasury Regulation 1.401(a)(9), Q&A-6, the “documentation” requirement stipulates that the IRA custodian must be provided with either a final list of all trust beneficiaries as of the September 30-of-year-after-death beneficiary determination date (including contingent and remainder beneficiaries and the conditions under which they would be entitled to payments) along with a certification by the trustee that all the requirements for stretch distribution are met under the trust. Or the trustee can simply provide a copy of the actual (irrevocable) trust document itself to the IRA custodian. Notably, while this is a purely administrative requirement, it is a requirement and does have a concrete deadline of October 31st of the year after death that must not be missed.

Under supporting Treasury Regulation 1.401(a)(9), Q&A-6, the “documentation” requirement stipulates that the IRA custodian must be provided with either a final list of all trust beneficiaries as of the September 30-of-year-after-death beneficiary determination date (including contingent and remainder beneficiaries and the conditions under which they would be entitled to payments) along with a certification by the trustee that all the requirements for stretch distribution are met under the trust. Or the trustee can simply provide a copy of the actual (irrevocable) trust document itself to the IRA custodian. Notably, while this is a purely administrative requirement, it is a requirement and does have a concrete deadline of October 31st of the year after death that must not be missed.

If the four requirements listed above are met, a trust as an IRA beneficiary can qualify as a designated beneficiary, and the post-death RMDs can be stretched, with the caveat that the stretch will still be calculated based upon the life expectancy of the oldest trust beneficiary of the trust (who would have the shortest life expectancy).