How Do Life Insurance and Qualified Retirement Plans Fit In?

The most important aspect of owning a Revocable Living Trust is ensuring that your assets are titled in the name of the Trust and therefore owned by the Trust.

The most important aspect of owning a Revocable Living Trust is ensuring that your assets are titled in the name of the Trust and therefore owned by the Trust.

There is an exception to this rule, that involves Qualified Retirement Plans (QRP’s), which include your IRA, 401(k), SEP, Keogh, 403(b) and even ROTH IRA’s. None of these vehicles can be “owned” by your Trust as that would cause them to become immediately taxable. Instead QRP's, just like life insurance, allow you to directly name primary and contingent beneficiaries.

When you are funding your Living Trust, you should also be reviewing any “direct beneficiary” type of accounts as well. In most cases, your overall plan for distribution of your total estate should be coordinated. Example: Are my IRA's and life insurance going to the same beneficiaries and in the same or similar fashion as in my Living Trust?

One way to ensure this is to name your Living Trust as the direct beneficiary of your IRA's and Life Insurance. But, is that always the best thing to do? The answer is NO, not always, and the decision can be more complicated than you might think.

Let's Take Life Insurance First

Ownership Issues: Life insurance may be owned by an individual or owned by a trust. Life insurance owned by a Revocable Living Trust will be included (death benefits) in the Settlor's estate for estate tax purposes. Life insurance owned in an Irrevocable Life Insurance Trust (a specific estate tax planning device) will not be included in the Settlor's estate at death. In either case policy death benefits are free from Income Taxation.

Ownership Issues: Life insurance may be owned by an individual or owned by a trust. Life insurance owned by a Revocable Living Trust will be included (death benefits) in the Settlor's estate for estate tax purposes. Life insurance owned in an Irrevocable Life Insurance Trust (a specific estate tax planning device) will not be included in the Settlor's estate at death. In either case policy death benefits are free from Income Taxation.

Consider that the owner of life insurance has specific rights, including access to cash values, and the ability to name and change beneficiaries. If an individual owner becomes incapacitated, then an agent under a durable power of attorney may be able to act in place of the owner. A Trust as owner will generally be recognized as having stronger legal authority with respect to the policy. If an individual owner should die, often, but not always, the named insured will usually become the owner of the policy with all rights inherent to ownership of the policy.

This may not always be the case, so you should check with the insurance company on their specific policy if an individual is to be named as policy owner. Also consider that, if the insured is a minor, incompetent or receiving public benefits assistance, it would not generally be prudent for such person to potentially become the owner of the policy.

There is no definitive right answer to the question of individual as owner or living trust as owner, so a review of the relevant facts and circumstances is advised before making the decision.

Beneficiary Issues: Life insurance claim payouts are income tax free whether paid out to an individual or a Trust. In most cases, naming your trust as the primary beneficiary of a life insurance policy is the smart move. It will benefit your spouse and/or other named Trust beneficiaries in the manner you have planned. It will protect minor children who are beneficiaries. It will provide possibly needed liquidity to pay debts or other bills so other estate assets don't have to be liquidated for that purpose, and it may even protect beneficiaries who are receiving public benefits assistance such as SSI or Medicaid. (Assuming your trust contains particular provisions for special needs beneficiaries and those receiving public aid.)

The main situation where naming your Trust as primary beneficiary would not be recommended is when your overall debts are near, or exceed, the value of your assets. In this case, naming individual beneficiaries to your life insurance policy will usually shield the proceeds from your creditors vs. having policy proceeds payable to your living trust which allows creditors easier access to those funds.

Next, the Qualified Retirement Plans

These are a little trickier, because these vehicles are taxable as money is withdrawn from them. Most people would like to defer the taxes as long as possible and sometimes defer any need to take withdrawals. A living trust can be an effective tool here but only usually if it contains very specific provisions. The provisions I am talking about are IRA Conduit Provisions. In order to be treated as a conduit or “see-through trust,” and qualify as a designated beneficiary, the trust must meet four very specific requirements, as stipulated in Treasury Regulation 1.401(a)(9)-4, Q&A-5.

Conduit provisions generally allow your Successor Trustee to make certain decisions for your beneficiaries including creating beneficiary IRA's for each qualifying Trust beneficiary. Unfortunately, not all estate planning attorneys include these provisions and without them, it is possible that the financial institution holding your IRA will treat this as a complete distribution to the Trust, all taxable at once.

You may want to spend a little extra time with your estate planning professional, investment advisor and tax professional to better understand your options. For most people without that inclination, it is often more productive and straightforward to name individuals in both primary and contingent beneficiary roles. If you are married, you would most often name your spouse as your primary beneficiary. He or she is permitted to complete an IRA Rollover from your IRA to their own IRA. Spouses as primary beneficiaries have the most tax efficient options available.

As for contingent beneficiaries, if you are naming your children, make sure they are adults, and that they are not receiving public benefits assistance such as Medicaid or SSI. Otherwise, consider naming your living trust as the contingent beneficiary and talk to your estate planning attorney to make sure your trust can manage all available options. Similar to what we discussed concerning life insurance, if individuals are directly named beneficiaries to your QRP's, then your creditors at the time of death will generally not be able to attach the QRP money designated for your children.

When directly naming beneficiaries to either type of account, ask questions to be sure you understand what your choices are. I have seen several clients show me beneficiary statements that list their spouse as primary beneficiary and then simply list all of their children with equal percentages by their names as the contingent beneficiaries.

I ask them if they are clear on what happens if their spouse and any of their children pre-decease them. Does that person's share go to your surviving children? Or does it go to the deceased child's spouse or their own children? That is generally uncertain, because now it will fall to the individual policy of the financial institution, and they don't all do the same thing. The benefit of naming a Trust sometimes is that contingent beneficiaries are usually clearly delineated.

In summary, here are some suggestions to discuss with your estate planning professional and investment advisor.

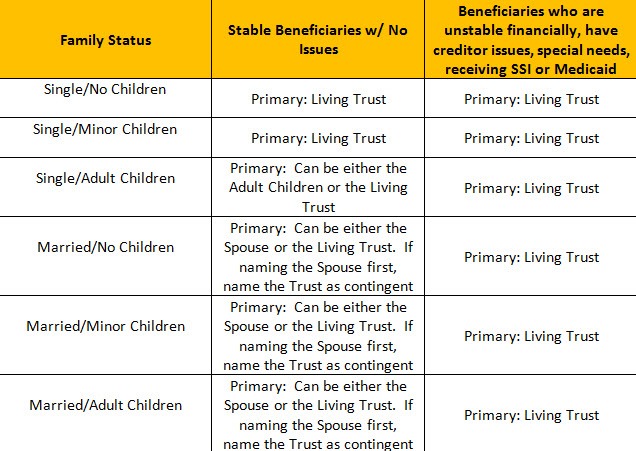

For Life Insurance

- If you have large debts in relation to your assets, a recommendation that will generally protect funds from your creditors would be naming adult beneficiaries as the Primary Beneficiaries.

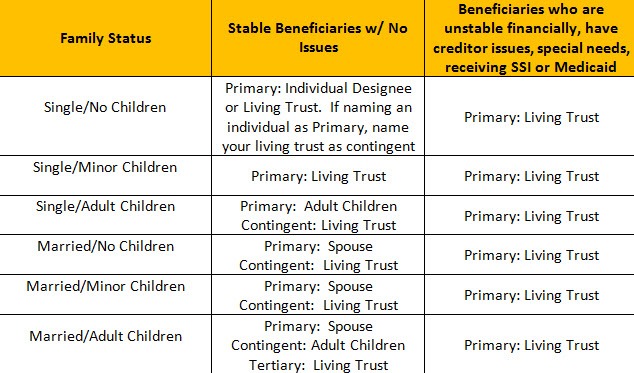

For Qualified Retirement Plans

- If you have large debts in relation to your assets, a recommendation that will generally protect funds from your creditors would be naming adult beneficiaries as the Primary Beneficiaries.

These recommendations are merely guidelines intended to help you ask the right questions and consider both yours and your intended beneficiaries circumstances so that you can make better decisions.