A Legal, Tax-Based Strategy for Deferring the Payment of Capital Gains Taxes

By Greg Reese, Certified Trustee for the Deferred Sales Trust

Today we begin our series of AmeriEstate articles covering the Deferred Sales Trust (DST) as a legal, tax-based strategy for deferring the payment of capital gains taxes. Greg Reese, AmeriEstate Legal Plan, Inc., President and CEO and Principal of Reef Point, LLC, will cover these topics in this and future articles:

- What are capital gains?

- What are the components of your assets for tax purposes?

- How does depreciation work?

- How are appreciated assets taxed upon sale?

- What is a Deferred Sales Trust (DST)? …with Sample case studies.

- How does the Deferred Sales Trust work?

- How are distributions taxed to the seller/taxpayer?

- Who offers the Deferred Sales Trust?

- Are you a candidate to establish a Deferred Sales Trust?

…and more

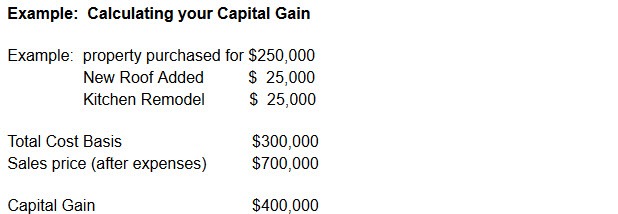

In short, capital gains are the difference between what you paid for something and what you sold it for. Many would refer to this as your “Profit.” When you sell an appreciated asset, the government taxes you on your profit. If you have not yet sold your asset, you have not generated a Capital Gain, and you wouldn't owe any taxes until that asset is actually sold. This also applies to assets you receive as a gift or assets that you receive as an inheritance. There is no tax due when you receive it, only when you sell it. Long-term capital gains carry reduced tax rates for assets held more than one year.

Cost Basis – This is what you paid for the property or other asset plus the cost of any capital improvements made to the property.

Depreciation – A unique tax treatment that allows you to deduct from income the depreciation or useful life of the property – e.g. the building itself is worth less the older it gets until, at some point, it will have to be replaced before it falls down. Depreciation expense, therefore, allows you to incrementally write off the future cost of having to replace the structure.

Real Estate has two components: The land, and any structures built upon the land.

Land does not wear out so it cannot be depreciated.

Buildings do wear out and can be depreciated. From a tax perspective, the IRS allows us to depreciate the portion of the property represented by the buildings on the land. In most cases, the seller is allowed to state that the buildings represent about 75% of the total value of the property and the land represents about 25% of the property. (There are slight variations to assigning percentages.)

LEARN MORE

Contact Us or call (800) 235-0963 to schedule an appointment with a DST Specialist.