Taking steps to defer your individual federal income tax bill is often a good idea. If you expect to be in the same tax bracket in future years, lowering this year's taxable income will postpone your tax bill and give you extra cash to work with until the bill comes due. If your tax rates turn out to be lower in future years, deferring taxable income into those future years will cause the deferred amounts to be taxed at lower rates.

However, in today's federal income tax environment, you could have “too much” deferral. Here are two big reasons why that might be the case.

1. Future Tax Rates Could Go Up

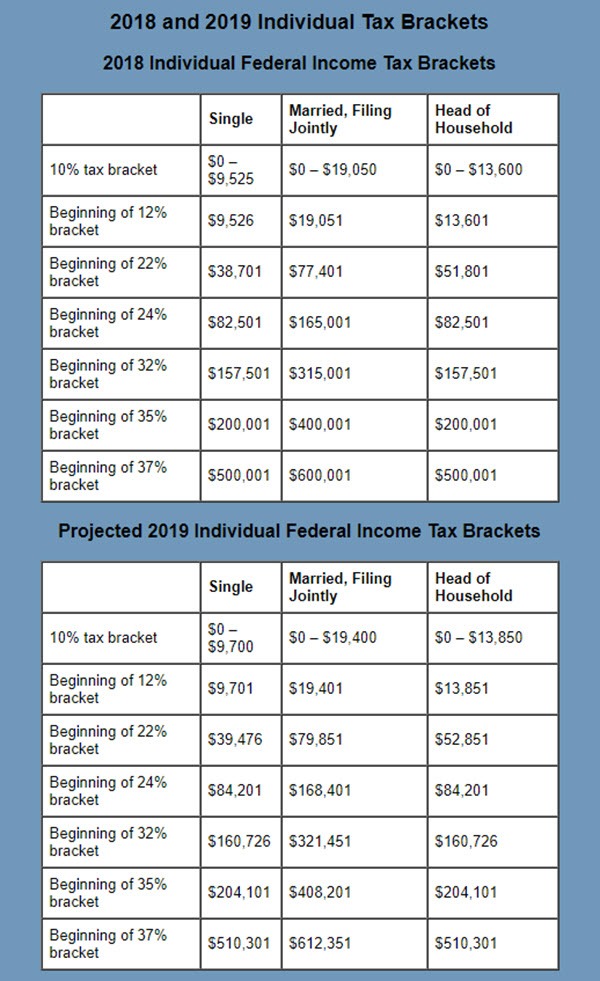

Thanks to the Tax Cuts and Jobs Act (TCJA), we know what the individual federal income tax rates and brackets are for this year and next year. (See “2018 and 2019 Individual Tax Brackets” below.) The 2020 brackets will probably be about the same as those for 2019, with modest adjustments for inflation.

But after 2020, we don't know if the TCJA's individual rates cuts will survive through 2025, as scheduled, or if they'll be revised by Congress. So, think twice about deferring income past 2020. Work with your tax advisor to project what might happen to your future tax bills in various scenarios.

2. Tax Deferral Could Negatively Affect QBI Deduction

The new deduction for up to 20% of qualified business income (QBI) from pass-through entities (including sole proprietorships) can't exceed 20% of your taxable income computed before any QBI deduction and net capital gains (net long-term capital gains in excess of net short-term capital losses plus qualified dividends).

So, tax deferral strategies that reduce taxable income — such as claiming first-year depreciation deductions or making large deductible retirement plan contributions — can potentially have the adverse side effect of reducing your allowable QBI deduction.

While most moves that defer taxable income just create timing differences for when income is recognized, the QBI deduction creates permanent tax savings. But it's scheduled to last only through 2025. So, beware of over-indulging on tax deferral moves if they would significantly reduce your QBI deduction. Also keep in mind that claiming first-year depreciation breaks will reduce your QBI and your QBI deduction.

Balancing Act

Determining the right amount of income to defer under today's tax law requires a delicate balance. Deferral strategies can still be an effective tax-planning strategy in the right situation and if used in moderation.

Small business owners have the most opportunities to defer taxable income. For example, small businesses that use the cash method of accounting for tax purposes might consider:

- Prepaying deductible expenses near year end,

- Sending invoices late enough to defer payment until the following year,

- Taking advantage of generous first-year bonus depreciation and Section 179 expensing deductions, and

- Making deductible contributions to retirement plans.

Thanks to changes included in the TCJA, many more small businesses are eligible for the cash method of accounting for federal income tax purposes. Before the TCJA, businesses with average annual gross receipts of more than $5 million for the previous three tax years generally weren't allowed to use the cash method. Under the TCJA, for tax years beginning after 2017, the gross receipts threshold has been permanently raised to $25 million.

Additionally, individuals who aren't small business owners can employ various strategies to defer taxable income. Examples of tax deferral techniques for individual taxpayers include prepaying expenses that give rise to itemized deductions, making installment sales of property, and arranging for like-kind exchanges of real estate.

Schedule Your Year-End Tax Planning Meeting

These ideas aren't a complete list of tax deferral opportunities. Your tax advisor can suggest other ways to lower your tax bill and can help craft the optimal overall tax planning strategy for your specific situation, taking into account the TCJA changes (including the QBI deduction) and the possibility of higher tax rates in future years.

Copyright: Thomas Reuters, Inc.